It seems that there is no objection to whether the Chinese economyis seriously declining. What is the economic growth in 2018? There are stillmany judgments. For example, the National Bureau of Statistics says it is 6.5%,Xiang Songzuo said that the estimate of an institution is 1.67%.The"Keqiang index" I calculated (Note 1) is 3.6%; and after correctingthe power generation of an important component of the "Keqiang Index"(Note 2), the "Keqiang Index" is about -1%. .The task now is toreverse the economic downturn. The policy for the right medicine shouldobviously be based on correct diagnosis. I have always stressed that becauseChina's urbanization process has not been completed, because China has a"major country effect" in international trade, we still have 15 to 20years of rapid economic growth. These two advantages have always been the basisfor our economic growth, bringing about an annual growth of 5 to 6%.Since thereis such a growth base, why is China’s economy going down in 2018? In my opinion, there are mainly four factors. The first is that thetax burden is too heavy, the second is the unfriendly to private enterprises,the third is the anti-urbanization policy (such as limiting the size of thecity), and the fourth is the violation and restriction of the network economy.For the first point, I have discussed in detail in the article "Thegovernment share is expanding, the profit margin will be exhausted". Onthe second point, I also discussed in the article "How to let privateentrepreneurs believe in the government"; on the reverse urbanizationpolicy, I also discussed in the article "The livelihood of the ordinarypeople, the foundation of big countries"; regarding the restrictions onthe network economy, I discussed the positive impact of the new economy in thearticle "Two Kinds of Economy in China". I will write an articledevoted to the negative impact of limiting the new economy. In addition, thereare two very important factors, one is the problem of state-owned enterprises,and the other is the issue of land system. The solution of these two problemswill bring about a growth rate of more than one percentage point of GDP, butthese two are long-term unresolved issues, not the main reason for the economicdownturn in 2018. It is clear what kind of policy should be adopted for these fourmajor issues. In view of the problem of excessive tax burden, large-scale taxreduction is required. For the problem of private enterprises, it is necessaryto improve the judicial system so that it can truly protect the legitimaterights of private enterprises. Regarding to anti-urbanization, it should stoprestricting the size of the city, this is a policy that directly offsets thepositive impact of the urbanization process; let the city open to all, andadopt other specific methods to solve the problem of insufficient singleresources in the city. As to the limits to new economy, it should be realizedthat the property rights formed by the network economy are also propertyrights. It is also necessary for it to obtain protection as property rights do,and to protect the network market as well as protecting the physical market. However, not all economists now agree with these four points, andthe resulting policy recommendations are very different. There are two verydifferent views on the excessive tax burden. One is to acknowledge that it isheavier than the Laffer Curve's best tax rate, but it is not a big problem, notthe main reason for the recession. The result of heavy tax burden is only tomake the income of enterprises and residents less, which leads to weakconsumption, but this can be compensated or replaced by expansionary macropolicies. The other, my opinion, is that the tax burden is too heavy, not onlyabove the optimal tax rate, but also to the point where companies can no longersurvive. That is, companies have no profit margins. These two different viewson tax burden have also led to different judgments on the nature of theeconomic downturn. The view that tax burden is not the main reason for theeconomic downturn argues that this economic downturn is similar to a cyclicalrecession, so it can be mitigated and hedged by counter-cyclical macroeconomicpolicy. The view that tax burden squeezes out profit margins argues thatenterprises will shut down or evacuated in a short period of time, leading toan avalanche-type economic downturn, rather than a cyclical problem, so taxcuts must be taken. See the figure below for specific logic.

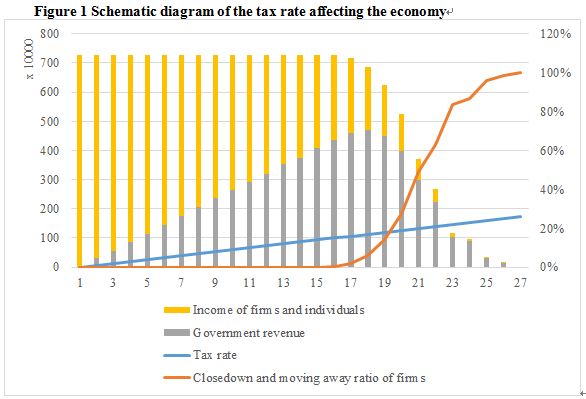

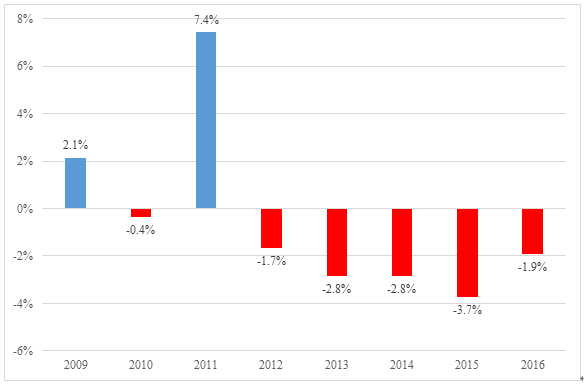

Description: This picture is only a schematic diagram. Thehorizontal axis represents time and the unit can be 1 year. Assume that overtime, the tax rate is gradually increasing (measured by the right-handcoordinates). For a long time, although the government's income is increasing,the income of enterprises and residents is decreasing, but it does not affectthe total social income. But after a certain high tax rate (16% here), thecompany began to shut down or evacuate, and showed acceleration, while thetotal social income fell like an avalanche. In the absence of profit margins, if only adopting an expansionarymacro policy, adding a counter-cyclical demand increase based on the totaldemand determined by the market will only partially increase the company’sorders, but due to the high tax rate, there is still no profit margin. If anenterprise increases the output of one unit, it can only increase one unit ofloss. The enterprise still has no incentive to expand production, and it cannotboost the economy from a macro level. Because the expansionary macro policy hasnot changed the distribution structure between the government and the corporateresidents, the enterprise is still in a situation where there is no money tomake. Others would say that the new demand from expansionary macroeconomicpolicies will reduce equipment idle rates and thus reduce average fix costs. Infact, since macroeconomic policy is only a countercyclical policy and is onlyadopted during a recession, the demand growth brought by this policy will notbring more demand than normal, and it will only reduce the equipment idle rateof the enterprise to normal status. The chart below shows the situation of thecapital “deserved income” (no risk interest rate + reasonable risk premium) ofprivate manufacturing listed companies. The chart shows that since 2012, theincome of the capital of these enterprises has not cover the loss, and thelength of time is close to a medium cycle. The loss that we see in the sense ofcapital “deserved income” is the loss under normal conditions, so expansionarymacroeconomic policies cannot fundamentally change the company’s lossexpectations. Figure 2 The part of theprivate equity manufacturing listed company's return on net assets minus the “deservedincome” from 2009 to 2016

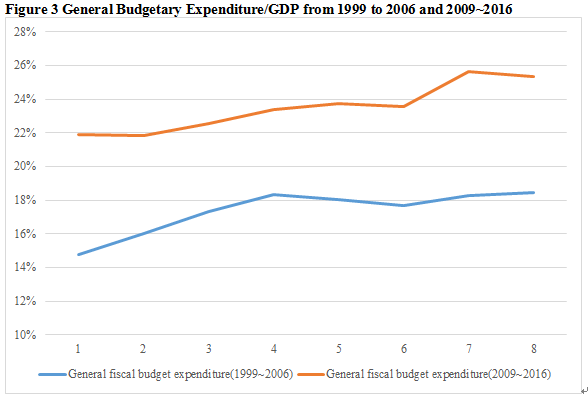

Explanation: This picture is a picture I used in my article,“Government's share expanding, profit margin will be exhausted”. This is thenet return on equity of privately companies in manufacturing minus therisk-free rate, minus the reasonable risk premium. The implication is that whenthis number is negative, the return on net assets is already lower than thereasonable return of capital. It should be noted that this data have beennegative for many years since 2012. If the economy declines severely in 2018,it may be a larger negative number. From 2012 to 2016, we should also regard itas “normal years”, so the expansionary macro policy can only pull the situationof the enterprise back to the “normal year” and cannot eliminate their losses. A more detailed analysis is that the expansionary macro policy willincrease the supplementary demand when the demand shrinks, and mitigate theimpact of the recession, but only reduce the fixed cost allocation, but cannotfully offset the fixed cost (depreciation + capital cost + management fee) )the apportionment. Because as mentioned above, capital has no reasonablereturn. At this time, although the company can regard the fixed cost alreadyinvested as the sunk cost, do not care, as long as the current price can makeup for the variable expenses, it can continue production. But entrepreneurswill not make new investments because capital is unprofitable. Thismacroscopically shows that expansionary macroeconomic policies can stimulateshort-term production growth, but cannot stimulate long-term productioncapacity increase, which cannot fundamentally solve the economic downturn.What's more, according to the theory of rational expectations, macroeconomicpolicies can only be "unexpected" and only work if the enterprisesand residents cannot foresee. If the government claims to adopt an expandedmacro policy in advance, the enterprise will not be bewildered by additionaldemand, and rashly take the decision to increase production capacity andinvestment, but raise prices. As a result, the economy has not grown, andprices have gone up. This is stagflation. Regarding the expansionary macro policy, when the economy isseriously declining, macro monetary policy will not actually have much effect.Because the money supply depends on the base currency and currency turnoverrate. The central bank can only affect the issuance of the base currency, andthe speed of currency turnover depends on the efficiency of the market systemand people's expectations. When people are generally pessimistic, the currencyturnover rate will slow down, thus offsetting the effect of the central bank'sexpansion policy. What's more, when the market system is weakened, the currencyturnover rate will also slowdown. In addition to this, it is the macro fiscalpolicy. We know that this is even more problematic. The first is that adoptingan expansionary fiscal policy requires more financial resources, which greatlyreduces the incentives for tax cuts. Second, as we saw in 2008, theexpansionary fiscal policy only emphasizes Increase demand without payingattention to the investment of financial resources and related efficiency. Onthe one hand, financial resources will rely on the channels of state-ownedenterprises, while the efficiency of state-owned enterprises is relatively low;on the other hand, in the context of government decision-making and emergencyresponse, financial resources are more likely to invest in the wrong directionor industry, resulting in further distortion of production structure. Some people will say that didn't the "four trillion"expansionary fiscal policy in 2008 avoid China's economic recession?Why can't it be done now? If "four trillion" still has theright place, then the timing is right. .Because it is only based on generalbudgetary expenditures, China's macro tax rate is 6.2 percentage points lowerin 2008 than it is now.(In this paper, the “macro tax rate” includes generalbudgetary expenditures, government fund expenditures, state-owned enterpriseopportunity income, and social security. Here, we assume that the proportion oflatter three parts in GDP is not changed, and treat the changes in generalfiscal budget expenditures as Changes in macro tax rates.) Going back 10 years,the macro tax rate from 1999 to 2006 is 5 to 7 percentage points lower than themacro tax rate from 2009 to 2016.See Figure 3.Therefore, at that time, thecapital gains of manufacturing enterprises were still above the “deservedincome”, capital was profitable, and enterprises were willing to expandproduction and investment.

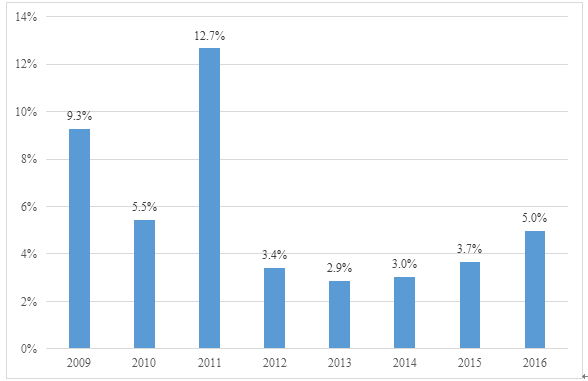

Note:Going back 10 years, the company has additional profitmargin which amounts to between theabove two lines, about 5~7%.In this picture, I put the general budgetaryexpenditure/GDP from 1999 to 2006 in the same period as the general budgetaryexpenditure/GDP from 2009 to 2016. We can visually see the gap in the macro taxrate over the past 10 years. Under such a tax rate, the company’s capital “deserved income” ismet. Most of the data in Figure 4 is the same as Figure 2, except that the taxrate 10 years ago was adopted .Therefore, the adoption of expansionarymacroeconomic policies 10 years ago not only increased orders, but alsoincreased profits, and also prompted enterprises to increase investment andproduction capacity, thus enabling China to avoid the economic recession in thecontext of the global economic crisis. However, today, when the macro tax rate is5-7 percentage points higher than 10 years ago, the so-called "fourtrillion" policy will no longer have the original effect. We can alsoconsider the data in Figures 2 and 4 as the basis for calculations whenentrepreneurs make decisions, and they calculate the expected return on theirinvestment by the average. The actual income is fluctuating around the expectedvalue. When the expected value is lower than the capital “deserved income”(Figure 2), they will not invest.

Figure 4 The portion of the private manufacturing listed company'sreturn on net assets from 2009 to 2016 calculated according to the macro taxrate from 1999 to 2006 is higher than the “deserved income”

Note: All the data in this figure are the same as in Figure 2,except correcting them by the difference between the existing macro tax rateand the macro tax rate 10 years ago.

Of course, many people have pointed out that the "fourtrillion" policy still has many drawbacks. Most people regard expansionarypolicies as demand policies. There has never been an isolated demand sidepolicy or a supply side policy. The expansionary fiscal policy is mainlyachieved by increasing government expenditures, including public worksexpenditures, and increasing the investment of state-owned enterprises.Therefore, the first is the impact on supply. Focusing on the stimulus todemand, because of the classic metaphor of Keynes's “pit-digging and filling”,people generally don't care what the government or state-owned companies arespending. In the implementation of expansionary fiscal policy, the governmentand state-owned enterprises are less concerned about whether the investmentprojects are economically reasonable, and they do not care whether they makemoney, so it is obviously much less efficient than the market-determinedinvestment, resulting in resource misplacement. .Once the direction andindustry were misdirected, it was difficult for the government and state-ownedenterprises to withdraw easily. This caused a serious imbalance in the supply structureand the so-called "overcapacity." This is not only a domesticeconomic issue today, but even an international economic issue. Obviously,adopting an expansionary fiscal policy will not only cannot solve the supplystructure problem, but will worsen it. Another view is to reduce taxes while adopting an expansionaryfiscal policy. The problem is that tax cuts require a reduction in fiscalrevenues, while expansionary fiscal policies require increased governmentspending; this will increase the fiscal deficit. This in itself will containthe tax cuts, making the tax cuts less than they should be. Even if the deficitis increased and the large-scale tax cuts and expansionary fiscal policies areimplemented at the same time, the large deficit itself will bring new problems,which will not only offset the benefits of the two measures, but also bringabout other damages. For example, there are two ways to hedge a deficit. One isborrowing, and the other is issuing money. For the government to borrow, there isa "Ricardo equivalent" proof that borrowing is only a delayed tax,and its effect is equivalent to taxation. Buchanan admits that there is still adifference between "taxation" and "deferred taxation". Thisis because modern people borrow money and let it is returned by futuregenerations, which will give people a "financial illusion" and thinkthat public goods are cheaper. But the result is that the government will belevied more taxes. What's more, the government's increase in borrowing has squeezedthe resources of the money market, which has led to an increase in interestrates, which has led to an increase in the financial costs of enterprises.Therefore, borrowing debt to expand fiscal policy will eventually offset thebenefits of tax cuts. The so-called "increasing currency" is the issuance of thebase currency above the reasonable rate of money growth, and the result isinflation. As mentioned earlier, in the early stages of the recession, due towidespread pessimism, the base currency issued could not effectively increasethe money supply. This has been proved by the facts of our country in 2018.From2018 to the present, the central bank has reduced the deposit reserve ratiofour times. By the end of the year, the loan balance increased by 13.5% fromthe end of the previous year, an increase of 2.6 trillion yuan over theprevious year, but the money supply (m1) increased only 0.005% by the end ofNovember. On this basis, the continued issuance of currency will not have asignificant effect in the short term. But these additional currencies willlurk, and jump out when the economy turns around and the currency turnoverspeeds up, bringing inflation. The depreciation of the currency brought aboutby inflation is equivalent to imposing an inflation tax on businesses andresidents. Nominal income appears to have increased, but production costs andconsumer goods prices have increased year-on-year and will be completelyoffset. Since there is a time lag between the issuance of money and inflation,since the issued currency flows from the government to the society throughstate-owned enterprises, the government and state-owned enterprises will eatmost of the inflation tax, and the private enterprises will increase the taxburden. .So choosing an inflation policy does not make a company enjoy a lowertax burden. The most important issue of the expansionary macro policy is that itis only a countercyclical policy. What we are facing now is not a cyclicalrecession, that is, the adjustment caused by some investment mistakes broughtabout by the economic upswing, but a big problem that most companies have noprofit margins. Therefore, our current task is not to counter-cyclical, but tocurb the economic collapse. If we can't prescribe the right medicine, we can't stopthe economy from continuing to decline. And as mentioned above, it may bringstagflation, further worsen the macroeconomic situation, and then when we wantto go back and implement tax cuts, it has delayed the timing and will have topay a higher price if it is to be corrected. Because it is followed by a crisisin the financial market due to problems in the real economy, leading to thebreak of the creditor's debt chain, and the rapid contraction of the moneysupply, which in turn will hurt the real economy, and the real estate marketwill also have a crisis, leading to a rapid economic contraction. Finally, itis the employment problem. In the past, China has to provide 10 million newjobs every year. If the economy is seriously declining, the employment problemis a very serious problem. And these problems have begun to appear now.Therefore, policy choices should not allow to be wrong. Therefore, only large-scale tax cuts can really reverse the economicdownturn. The so-called large-scale, I have proposed that the value-added taxshould be reduced by more than 3 percentage points, and the corporate incometax should be reduced by more than 5 percentage points; overall, the macro taxrate should be reduced by more than 4 percentage points. This is equivalent to4 trillion yuan. It can't be called "mass tax cuts" if it is reducedby several hundred billion yuan. The core role of large-scale tax cuts is togive enterprises and residents a clear profit margin by giving a strong signal,so that they have incentive to invest. This is an action to expand long-termeffective production capacity. Tax cuts themselves will increase the currentincome of enterprises and residents by changing the distribution ratio, therebyincreasing the current total demand, but the greater demand brought by tax cutsis actually the investment demand brought by the optimistic expectations ofsuch enterprises, and the recovery from the market transactions and theincrease in revenue generated from the market. This kind of income is thehealthiest, most mainstream, largest, and most market-dependent income, becauseit shows that the company's products are marketable products that meet the realneeds of the market. It is a reward for making the right decisions aboutproduction and investment. As mentioned earlier, tax cuts, although referred to as “supplypolicies”, actually bring about an increase in the total health demand. Saysaid that “supply itself brings demand”, and Steven Cheung goes further andsays “people supply for their demand” , this relies on an effective and maturemarket. Only when the transaction is voluntary, the price signals formed bymany transactions are not distorted, enterprises and residents make productionand consumption decisions based on price signals, and supply will directlybecome income, and income will directly become demand. Therefore, as a supplypolicy, tax reduction requires simultaneous market-oriented reforms and reducedgovernment intervention. Another self-evident consequence of tax cuts is the needto streamline government institutions. The main reason why China is currentlyweakening the market system, distorting the price signal, and intervening inthe behavior of market entities is that the government departments are toolarge. If we streamline 90% of the administrative permissions, streamline thosegovernment departments that have a negative effect on the market, andstreamline the overly bloated administrative agencies, we can greatly reduceintervention to market, and threats to and violations of corporate propertyrights. At the same time, solve the problem of being unfriendly to privateenterprises. Tax cuts will not bring about fiscal deficits caused by expansionarypolicies, inflation, and crowding out money resources, so it is a policy withlittle side effects, health and cleanliness. It will also significantly speedup the economy, so the tax cut is lower than the tax-rate cut (ie, lower thanthe aforementioned 4 trillion yuan).It has only one weakness, that is, thegovernment administration may not like it. Because tax cuts are a reduction inthe amount of resources that government administrations may control, this is atleast intuitively detrimental to these sectors. The expansionary fiscal policyrequires increasing the resources that the government's administrativedepartments must control, and at the same time increasing their power andinterests. As a result, expansionary fiscal policy is more likely to be asubstitute for tax cuts for macro decision makers. But the hope that the expansionarymacro policy works will only be a desire. What is actually going to happen islikely to be as described in this article, which will quickly lead to adeterioration of the situation. Only those who have a vision beyond theimmediate interests of the executive branch, and who have the mind andforesight, can take drastic tax cuts. At the end of last year, the Politburo ofthe Communist Party of China proposed to "reducing taxes and reducing feeson a larger scale." We will see what "larger scale" means. ———— Note 1: The three components of the “Keqiang Index” in this paperare: by November 2018, the growth rate of cargo turnover (3.4%, weight 25%),the growth rate of money supply (m1) (0.005%, Weight 35%), power generationgrowth rate (6.9%, weight 40%). Note 2: This is a correction based on data provided by myauthoritative friend. The corrected power generation growth rate is -4.7%. January 5, 2019 in Fivewoods house Published firstly in FT Chinese and China-review Weekly

|